P Navigating the complex world of healthcare can be challenging, especially when choosing the right health insurance plan. The Massachusetts Health Connector (MA Health Connector) offers various plans to fit diverse needs and budgets. This article delves into expert perspectives and practical insights to help you make an informed decision regarding your health insurance through MA Health Connector.

Key Insights

- Primary insight with practical relevance: Understanding the types of plans offered by the MA Health Connector can significantly influence your healthcare decisions.

- Technical consideration with clear application: Recognizing the differences between Platinum, Gold, Silver, Bronze, and Catastrophic plans will help in selecting the most appropriate coverage.

- Actionable recommendation: Leverage the online tools and resources provided by the MA Health Connector to compare plans and estimate costs.

Understanding Different Plan Tiers

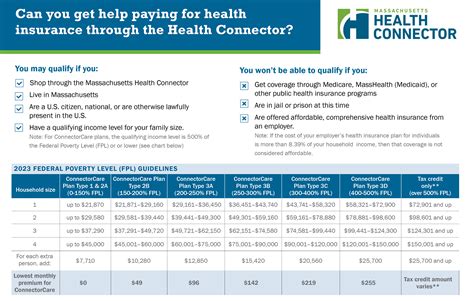

MA Health Connector offers plans categorized into four main tiers: Platinum, Gold, Silver, and Bronze, each differing in cost, coverage, and out-of-pocket expenses. The Platinum plans have the lowest out-of-pocket costs and highest premiums but provide extensive coverage. They are ideal for those who prefer comprehensive coverage without worrying about deductibles. On the other end, Catastrophic plans have the lowest premiums but highest out-of-pocket costs and are suitable for young, healthy individuals who rarely need medical care.

In the middle, the Gold and Silver plans strike a balance between cost and coverage. Gold plans typically have lower premiums but higher out-of-pocket costs compared to Silver plans, making them a versatile choice for most individuals and families. Silver plans offer more affordable premiums and a slightly higher deductible, making them a balanced option for those looking for a middle ground between cost and coverage.

Choosing the Right Plan for You

Selecting the right plan through the MA Health Connector is not just about choosing the cheapest option. It requires a careful assessment of your healthcare needs, budget, and long-term financial goals. Begin by estimating your annual medical expenses, including doctor visits, medications, and any anticipated procedures. This will help you gauge which plan’s out-of-pocket costs will be most manageable for you. Moreover, consider factors such as access to preferred healthcare providers and the network’s extensiveness. Ensuring your primary care physician and specialists are part of the plan’s network can significantly reduce out-of-pocket costs.

Utilize the plan comparison tools available on the MA Health Connector website to visualize the details of each plan, including premiums, deductibles, copayments, and out-of-pocket maximums. This tool allows you to make a data-driven decision, tailoring your selection to meet your specific healthcare requirements and financial circumstances.

Can I change my health plan after enrolling?

Yes, you can change your plan during open enrollment periods or during a qualifying life event such as marriage, birth of a child, or loss of other health coverage. It's crucial to review your options and make changes accordingly to ensure continuous coverage and financial protection.

What if I miss the enrollment deadline?

If you miss the standard enrollment period, you may still be able to get a plan if you experience a qualifying life event. Special enrollment periods provide a window of opportunity to purchase health coverage outside of the standard open enrollment period, allowing you to adjust your coverage based on life changes.

In conclusion, selecting a health insurance plan through the MA Health Connector involves understanding the different tiers and making informed decisions based on your healthcare needs and financial situation. Utilizing the resources available and leveraging comparison tools will facilitate a well-informed choice, ensuring you receive the best possible healthcare coverage for you and your family.