If you’re searching for a health care solution that offers flexibility and immediate coverage without the long-term commitment, short term health care plans might be an ideal fit. They’re designed to bridge gaps in coverage, offering affordable and accessible health insurance options that cater to temporary needs. This guide aims to provide you with a comprehensive understanding of short term health care plans, offering practical advice to help you make informed decisions.

Understanding Short Term Health Care Plans

Short term health care plans are temporary insurance solutions that provide coverage for a limited period—typically ranging from a few weeks to up to 36 months, depending on the provider. They are specifically designed for individuals who require health coverage for a short duration, such as between jobs, until a new health insurance plan takes effect, or during unexpected gaps in coverage. Despite their temporary nature, they cover essential health services to ensure you’re not left without necessary medical care.

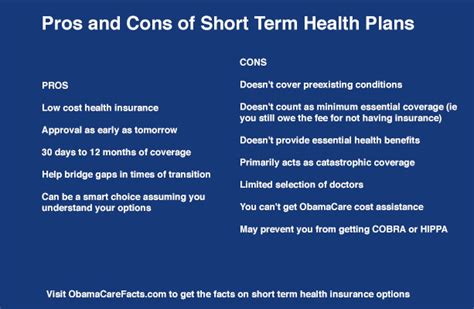

When considering short term health care plans, it’s important to understand both their advantages and limitations. These plans tend to have lower premiums compared to standard health insurance policies, but they often come with higher out-of-pocket costs and might not cover pre-existing conditions or some essential health benefits as mandated by comprehensive health plans.

Key Benefits of Short Term Health Care Plans

Short term health care plans offer several benefits, particularly for those in temporary or transitional phases of life. Here’s an overview of why they are a compelling choice:

- Affordability: Typically, the premiums for short term health care plans are lower than those for standard health insurance plans, making them a cost-effective solution for short-term needs.

- Flexibility: These plans are ideal for those who do not qualify for other insurance programs due to gaps in employment or until a new health plan becomes available.

- Access to Immediate Coverage: Most short term health care plans offer immediate coverage as soon as you enroll, providing peace of mind without waiting periods.

Potential Drawbacks

While short term health care plans have many benefits, it’s important to consider their limitations to ensure they meet your specific health care needs:

- Limited Coverage: These plans may not cover all necessary health services, especially pre-existing conditions and some preventive care measures.

- Higher Out-of-Pocket Costs: Due to the lower premiums, out-of-pocket costs, like deductibles and co-pays, are often higher.

- Short Duration: Coverage is temporary and may not be renewed indefinitely, which could leave you uninsured if you remain in a gap situation.

Immediate Actions to Take When Choosing a Short Term Health Care Plan

To ensure you make an informed decision when selecting a short term health care plan, here are immediate steps you should take:

Quick Reference

- Immediate action item with clear benefit: Compare multiple short term health care plans to find the best fit for your budget and medical needs.

- Essential tip with step-by-step guidance: Review the terms and conditions of the plan thoroughly before enrolling to understand coverage, exclusions, and limitations.

- Common mistake to avoid with solution: Don’t ignore the fine print that outlines what is not covered; this can save you from unexpected out-of-pocket expenses.

Detailed How-To: Comparing Short Term Health Care Plans

Choosing the right short term health care plan involves careful consideration and thorough comparison. Here’s a detailed guide on how to compare different short term plans:

Step 1: Define Your Needs

Start by identifying what health services you need coverage for. Consider your regular health care requirements, including any prescription medications, doctor visits, emergency care, and hospital stays. This will help you compare plans based on what’s most important to you.

Step 2: Research Providers

Look for reputable insurance providers that offer short term health care plans. You can find this information through online reviews, consumer reports, and professional advice from insurance agents. Ensure the providers have a good track record of claims handling.

Step 3: Evaluate Plans

When evaluating different plans, consider the following factors:

- Premiums: Compare monthly premiums to ensure they fit within your budget.

- Deductibles and Co-pays: Understand the out-of-pocket costs for medical services. Higher premiums often mean lower deductibles, and vice versa.

- Coverage Limits: Ensure the plan covers essential services, such as emergency care, primary care, and prescriptions.

- Exclusions and Limitations: Carefully review what is not covered under each plan. This includes any specific conditions, services, or types of care that are excluded.

Step 4: Check Renewal Policies

Short term plans often come with a maximum duration, sometimes with the option to renew. Understand the renewal process and the conditions under which you can continue coverage.

Detailed How-To: Enrolling in a Short Term Health Care Plan

Once you have identified the most suitable short term health care plan, the next step is to enroll in it. Here’s a comprehensive guide on the enrollment process:

Step 1: Gather Required Information

Before enrolling, you’ll need to gather personal information, including proof of identity, contact information, and possibly medical history. Ensure you have these documents ready.

Step 2: Visit the Provider’s Website

Navigate to the insurance provider’s official website. Most providers offer online enrollment, making the process more convenient and faster.

Step 3: Complete the Enrollment Form

Fill out the online enrollment form with accurate and complete information. This includes personal details, plan selection, and any required documents.

Step 4: Pay the Premium

After submitting the enrollment form, you will need to pay the premium. Most plans accept various payment methods, including credit cards, bank transfers, or other online payment systems.

Step 5: Confirmation and Coverage Start Date

Once your application and payment are processed, you will receive a confirmation and details about your coverage start date. It’s important to review your policy documents carefully.

FAQs on Short Term Health Care Plans

What medical services are covered by short term health care plans?

Short term health care plans generally cover essential health services, including primary care, emergency care, hospital stays, and preventive care. However, it’s important to note that these plans may not cover all medical services or pre-existing conditions. Before enrolling, thoroughly review the coverage details to ensure they meet your specific health care needs.

Can short term health care plans be renewed?

Yes, many short term health care plans offer renewal options, typically up to a maximum of 36 months. However, renewal policies vary by provider, and some plans may not allow for unlimited renewals. Check the terms and conditions of the plan you select to understand the renewal process and any conditions that apply.

Are short term health care plans suitable for people with pre-existing conditions?

Short term health care plans often do not cover pre-existing conditions. This is one of the key limitations of these plans compared to comprehensive health insurance policies. If you have known health issues, it’s advisable to look into other health care options that offer coverage for pre-existing conditions or consider maintaining existing coverage until you find a more suitable long-term plan.

Navigating short term health care plans can be straightforward if you approach it with a clear understanding of your needs and a methodical evaluation process. With this guide, you’re equipped with actionable advice, practical examples, and detailed steps to make an informed decision that fits your temporary health care needs